When you pick up a prescription, the price isn’t just about the pill inside—it’s shaped by medication costs, the total out-of-pocket expense for a drug, including what insurance covers and what you pay directly. Also known as prescription prices, these costs are influenced by patents, manufacturing, insurance rules, and even where you live. You might pay $5 for a generic blood pressure pill one month and $300 for a brand-name cancer drug the next, even if they treat similar conditions. That’s not random—it’s the system at work.

Generic drugs, medications that are chemically identical to brand-name versions but sold without the original patent, are supposed to cut costs dramatically—often by 80% to 95%. But not all generics are treated the same. Insurance formulary, the list of drugs your plan prefers and covers at lower costs, determines which generics you can get cheaply and which ones require prior authorization or higher copays. Some insurers push you toward certain brands or generics because they get rebates from manufacturers, not because they’re better for you. Meanwhile, copay assistance, programs that help patients pay part of their prescription bills through nonprofits or drugmakers, can reduce your monthly expense by hundreds of dollars—if you know where to look. Many people don’t realize they qualify for help because they assume it’s only for the poor. In reality, even people with insurance often pay too much because their plan has high deductibles or narrow networks.

Why do some drugs stay expensive even after patents expire? Sometimes it’s because the manufacturer delays generic competition by filing lawsuits or paying generic makers to wait. Other times, it’s because the drug is hard to make—like complex biologics or specialty injectables—so fewer companies can produce them. That’s why you’ll see articles here about the Purple Book, tentative FDA approval, and how pharmacy benefit managers control access. These aren’t just buzzwords—they’re the hidden gears behind your pharmacy bill.

You’ll find real examples here: how smoking cuts clozapine levels by half, forcing dose changes that affect your wallet; why insurers prefer preferred generic lists that save them money but leave you with fewer options; and how Medicare Extra Help can lower your monthly costs even if you think you earn too much to qualify. We cover what actually works—not just theory, but what patients are doing right now to avoid overpaying.

Whether you’re managing diabetes with sulfonylureas, treating depression with antidepressants, or taking oral chemo at home, your medication costs don’t have to be a surprise. The information below gives you the tools to ask the right questions, spot hidden fees, and find real savings—without guessing or hoping for the best.

Posted by

Jenny Garner

8 Comments

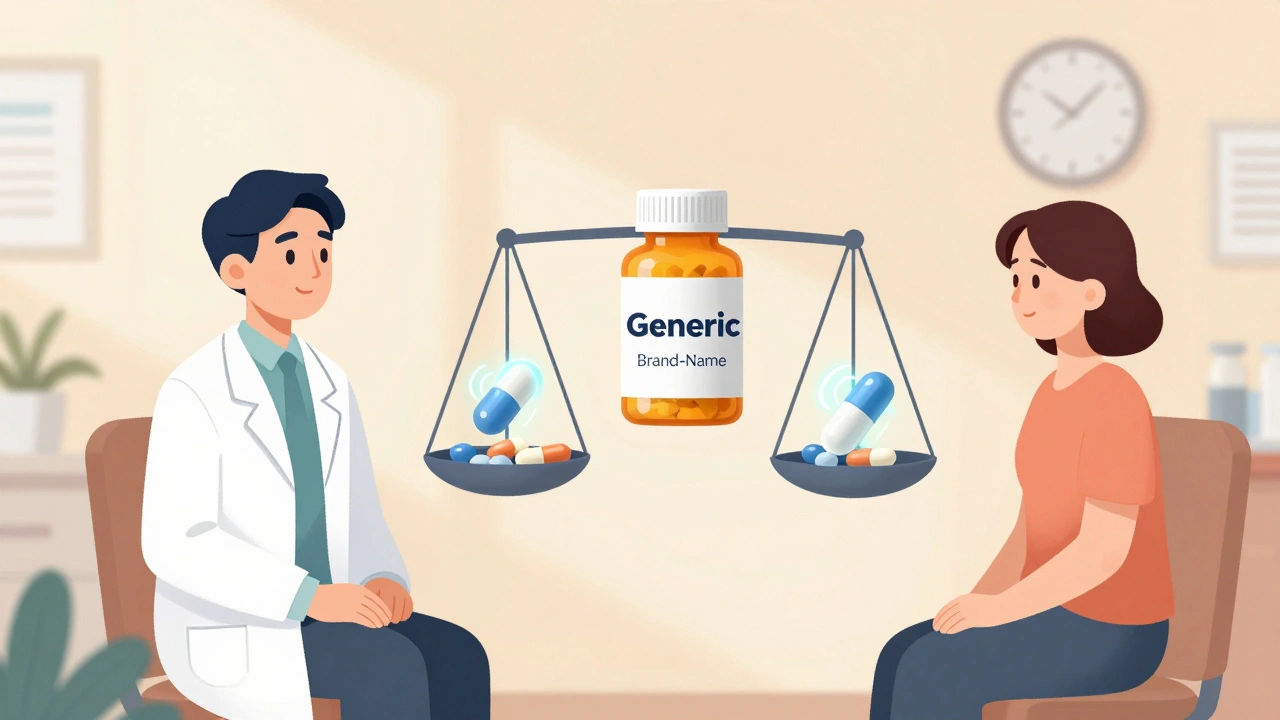

Learn how to talk to your doctor about generic vs. brand-name medications-when generics work just as well, when to ask for the brand, and how to save money without risking your health.

read more